Find Your Perfect Mattress with Our Guides

Is Financing Furniture a Good Idea? Your 2026 Guide

You’re probably asking this because the timing isn’t perfect.

Maybe you just bought a house in LaGrange. Maybe you’re moving into a bigger place in Troup County. Maybe your old sofa has finally given up, the guest room is still empty, and you need a real mattress instead of “making do” for one more month. Furniture is expensive, and when you’re trying to furnish a full home, the total adds up fast.

So, is financing furniture a good idea?

My answer is simple. Yes, sometimes. No, often. It’s a smart tool when it helps you buy lasting quality on terms you fully understand. It’s a bad idea when it lets you overspend, ignore the fine print, or finance something disposable that won’t outlast the payments.

If you want the shortest possible advice, here it is: finance furniture only when the piece is worth owning for years, the monthly payment fits your real budget, and the terms are clean. If those three things aren’t true, walk away.

Understanding Furniture Financing Options

Furniture financing just means you take home the furniture now and pay for it over time instead of all at once.

That can be a practical move. Furniture isn’t a random impulse purchase for most families. It’s a home expense, and often a meaningful one. According to a Provoke Insights furniture financing survey, 30% of Americans who purchased furniture in the last year used financing options in Fall 2022/Winter 2023. The same survey found financing use was higher among parents at 34% and millennials at 35%. That tells you this isn’t unusual. It’s a mainstream way people handle home purchases.

The common financing choices

Most shoppers run into a few basic options.

In-store promotional financing

This is the classic offer. You’ll see terms like 0% APR financing for a set period. That can be appealing if you know you can clear the balance before the promotion ends.Buy now, pay later plans

These plans break the purchase into smaller payments. They’re popular because they feel straightforward and less intimidating than opening a traditional store account.Store credit cards

These often come with promotional offers, but they also require more caution because the terms can get expensive if the balance lingers.Personal budget-first saving

This isn’t financing in the technical sense, but it competes with financing. Some shoppers delay the purchase, save up, and pay in full.

What financing should do for you

Good financing doesn’t magically make furniture affordable. It changes the timing.

That matters when the goal is buying the right piece instead of settling for the cheapest one in stock. A family replacing a worn-out sofa may decide that spreading payments makes more sense than buying a lower-quality piece that needs replacing too soon.

Practical rule: Financing should help you buy better, not simply buy more.

If you’re comparing plans, start with the basics. What is the monthly payment? Is the rate promotional or standard? Is there any deferred interest language? Can you pay early? Those questions matter more than the sales sign.

If you want to review how furniture payment plans are typically presented, take a look at furniture financing options. Even if you’re still deciding, seeing the structure helps take the mystery out of it.

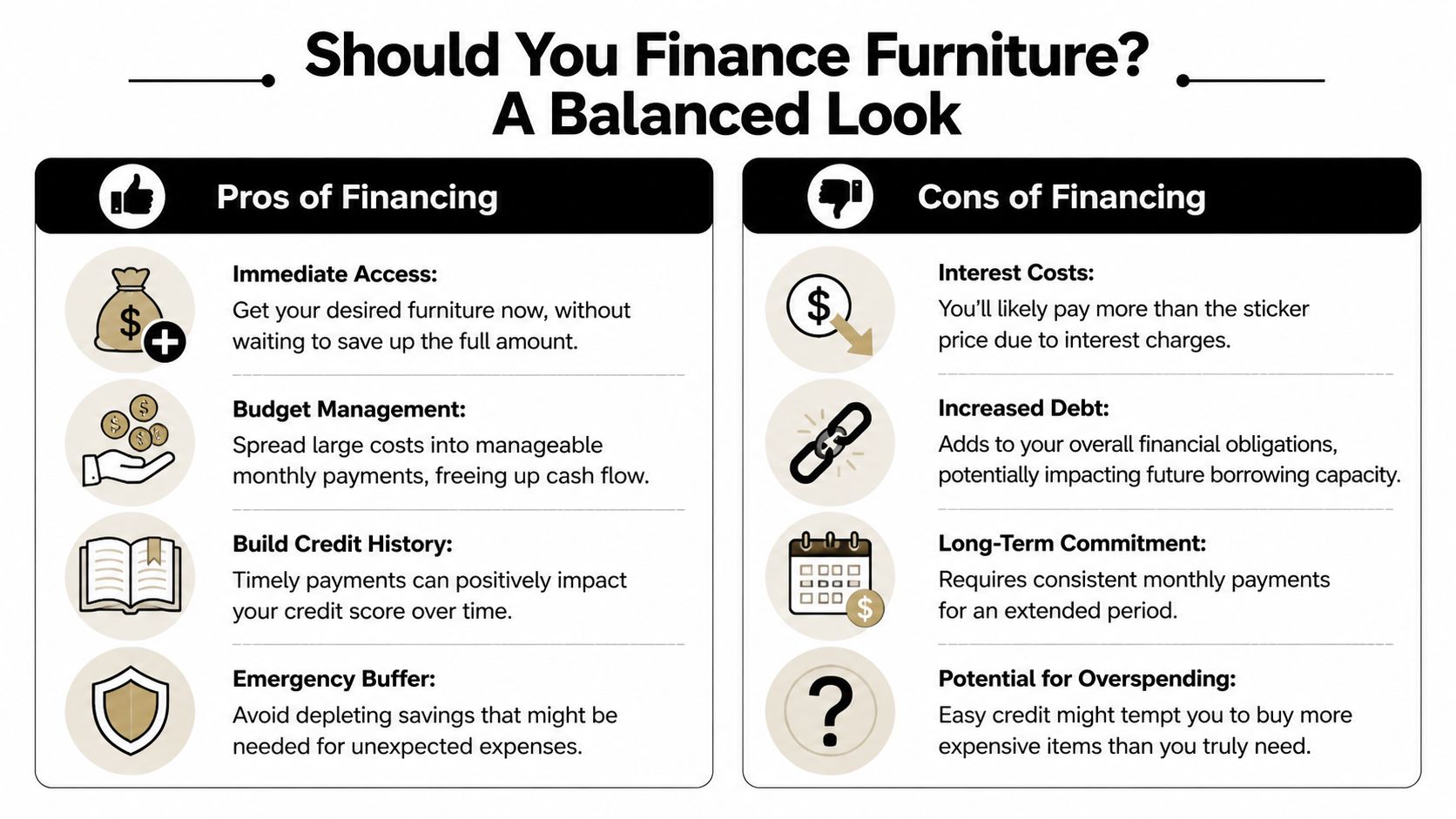

Weighing the Pros and Cons of Financing

Financing furniture can be a good idea. It can also be one of the easiest ways to turn a sensible purchase into an expensive regret.

The deciding factor isn’t whether financing exists. It’s whether the financing supports a smart purchase. If you’re buying furniture built for generations, not just a few seasons, financing can help you get there. If you’re using monthly payments to justify an overpriced impulse buy, it’s working against you.

When financing makes sense

The best use of financing is simple. You need the furniture, you expect to keep it for years, and you can handle the payment comfortably.

A strong example is a bedroom set, a quality mattress, or a living room sectional that gets used every day. For purchases like that, spreading the cost can protect your cash while still letting you invest in comfort and durability.

Here’s where financing can work in your favor:

You keep cash on hand

Paying over time can preserve savings for moving costs, repairs, school expenses, or the ordinary surprises that show up in real life.You can buy quality now

Sometimes the cheaper piece is the more expensive mistake because you replace it sooner. Financing can help you step into better materials, stronger construction, and better comfort.You may get a promotional rate

According to this review of furniture financing promotions, furniture financing is most advantageous during 0% APR promotions, often offered for 6-48 month terms, because the retailer covers the interest. That only works if you pay the balance off before the promotional period ends.You can furnish a room in one move

That matters more than people admit. Buying one piece now, another much later, and a third when something goes on sale often creates a room that never quite feels finished.

When financing is a bad idea

Financing becomes a problem when it lets emotion outrun judgment.

You see a beautiful sectional. The monthly number looks manageable. You focus on the payment instead of the full cost. That’s where people get in trouble.

Watch for these warning signs:

You’re choosing based on payment, not value

If you don’t know the full price, the term length, and the rate, you’re shopping blind.The purchase stretches your budget

A monthly payment that looks fine on a calm month may feel very different after a car repair, school expense, or medical bill.You don’t understand the promotion

A financing offer isn’t a bargain just because it says zero interest in large print.The furniture isn’t worth financing

I’m opinionated on this. Don’t finance throwaway furniture. Finance pieces that will still make sense in your home years from now.

If you need financing to buy low-quality furniture, the real problem usually isn’t the financing. It’s the furniture.

My recommendation

Use financing for high-use, lasting pieces. Be cautious with trendy pieces. Avoid financing for filler furniture, short-term fixes, or something you’re already unsure about.

That’s especially true when you’re shopping for things like:

- Living room sectionals

- Serta mattresses

- Bassett recliners

- Solid wood dining furniture

- Custom furniture with specific fabrics or finishes

Those are purchases where quality, comfort, and fit matter. They’re home investments, not quick transactions.

The True Cost of a Financed Sofa A Real-World Example

Let’s make this concrete.

A family in LaGrange needs a new living room sectional. The old one is sagging, the seats are uneven, and they’d rather buy one good piece than go cheap and replace it again. They’re looking at a $3,000 sectional and trying to decide whether financing is a good idea.

The answer depends entirely on how they pay.

Four ways the same sectional can cost very different amounts

The biggest trap in furniture financing is deferred interest. That’s the clause many people miss because the promotion sounds simple. But if the balance isn’t paid in time, interest can be applied retroactively.

According to MyBankTracker’s explanation of deferred interest on furniture financing, promotional 0% APR offers often include a deferred interest clause. If the balance isn’t paid off before the promotion ends, rates averaging 25-30% APR can be applied retroactively to the original purchase amount, adding hundreds of dollars in fees.

That’s why a good financing plan and a bad one can start out looking identical.

Cost comparison for a $3,000 sectional purchase

| Payment Method | Monthly Payment | Total Interest Paid | Total Cost |

|---|---|---|---|

| Cash upfront | $0 monthly after purchase | $0 | $3,000 |

| 24-month 0% APR, paid in full on time | $125.00 | $0 | $3,000 |

| 24-month promo, balance not paid before deferred interest triggers | Varies | Could add hundreds in fees | More than $3,000 |

| Standard credit card | Varies | Interest continues until paid off | More than $3,000 |

The cleanest financed version is obvious. A 24-month 0% APR plan works if the buyer pays $125.00 per month and finishes on time.

That’s the key. Not almost on time. Not “close enough.” On time.

What shoppers often miss

People get distracted by the showroom moment. The room will look finished. Delivery is handled. The sofa solves a real problem. All of that is fine.

The mistake happens when the buyer says, “I’ll pay extra later,” without a hard plan. Life gets busy. The balance hangs around. Then the promotion ends, and the so-called deal becomes a costly lesson.

Bottom line: Promotional financing is only cheap when your payoff plan is already settled before you sign.

That’s why I prefer buyers to work backward from the calendar. If the term is two years, divide the purchase by the number of months and ask one hard question: “Will I really pay this every month without fail?”

If the answer is shaky, either shorten the purchase, raise the down payment, or choose another route.

You can also preview how installment plans are framed by browsing monthly furniture payment options. The monthly number should support your budget, not seduce you into ignoring the full obligation.

Financing Versus Other Payment Options

Financing isn’t the only way to buy furniture, and it isn’t automatically the best one.

The better question is this: which payment method fits the type of purchase you’re making? Buying a quality sofa for the long haul calls for one kind of decision. Picking up a temporary side table for a spare room calls for another.

Paying cash

Cash is the simplest option. It’s clean, final, and usually the cheapest way to buy because there’s no ongoing payment hanging over you.

But cash has a weakness too. It can push shoppers toward a lower grade of furniture just to stay inside an immediate budget. That’s not always wise. If paying cash means buying something flimsy instead of a durable American-made furniture piece that will hold up well, the “cheaper” choice may not be the better value.

Cash works best when:

- You already have the funds and won’t wipe out your emergency cushion

- The purchase is modest and doesn’t crowd out more important needs

- You’re disciplined enough not to settle for a poor-quality substitute just because it’s available today

Using a credit card

A regular credit card is convenient, but I don’t love it for big furniture purchases unless the payoff plan is immediate.

Credit cards make it too easy to carry a balance, and once that happens, the furniture keeps costing you long after the excitement is gone. For an everyday-use purchase like a sofa, recliner, or mattress, that’s a rough way to pay.

A credit card is usually a better fit when:

- you’re making a smaller purchase,

- you’ll pay it off quickly,

- or you’re using it for convenience rather than long-term borrowing.

Layaway and waiting

Some shoppers still prefer the old-fashioned route. They save, place items on hold if available, and buy only when the money is ready.

That takes patience, but it has real benefits. You avoid debt, you get time to think, and you’re less likely to make a rushed choice. The downside is obvious. You may wait a long time with an uncomfortable room, an old mattress, or a space that never quite comes together.

Which option fits which goal

Here’s the practical comparison.

- Cash is best for shoppers who want the lowest-risk path and already have the money.

- Financing is best when you’re buying lasting quality and have a clear payoff plan.

- Credit cards are best for short-term convenience, not long-term furniture debt.

- Layaway or waiting is best when the purchase isn’t urgent and you’d rather avoid monthly obligations.

Buy based on the lifespan of the furniture, not the emotion of the moment.

If your goal is a short-term fix, don’t turn it into a long-term payment. If your goal is a serious home upgrade, financing can be a practical tool. For shoppers comparing installment-style plans, buy now pay later furniture options can help you understand the structure before you commit.

That’s the lens I’d use in LaGrange, West Point, Pine Mountain, or Hogansville. Match the payment method to the quality level and the years of use you expect from the piece.

A Decision Guide for Your Home and Budget

Different buyers should make different financing decisions.

A newly married couple furnishing a first house doesn’t face the same choice as a family replacing worn living room seating, and neither of them is in the same spot as someone moving quickly for work. You need a decision that fits your home, your budget, and your credit profile.

For the first-time homeowner

If you’ve just bought your first place in LaGrange, financing can help you furnish essential rooms without draining every dollar you’ve got. That part makes sense.

The caution is credit. According to this summary of credit score effects tied to furniture financing, a 2023 TransUnion study notes that new retail accounts can initially drop FICO scores by 10-20 points, and a single missed payment can lower a score by over 90 points. If your credit file is still thin, that matters a lot.

So my advice is firm:

- finance only the rooms you need now,

- keep the payment modest,

- and never open an account unless you already know how it fits into the rest of your bills.

For the growing family

Families usually need durability more than novelty.

Financing can help if you’re replacing multiple high-use pieces at once, such as a sofa, recliner, or mattress. Kid-friendly fabrics, comfortable support, and better construction usually cost more up front, but they tend to make more sense over the life of the furniture.

Good candidates for careful financing include:

- Bassett recliners for everyday use

- Living room sectionals that anchor the main family space

- Serta mattresses when better sleep is a household priority

- Solid wood pieces that can handle years of use

Families should be extra strict about one thing. Don’t finance decor-level upgrades while calling them necessities. Finance comfort, function, and longevity first.

For the new mover

Moving compresses decisions. You need a bed now. You need seating now. You may need a dining setup now. That urgency can make financing feel more attractive than it should.

Use it selectively.

Start with the pieces that affect daily life the most. A mattress, a sofa, and one practical eating surface come before accent pieces, extra storage, and “nice to have” additions. If you finance everything at once, the room may look complete, but the budget can feel strained for a long time.

Furnish in layers if you need to. Comfort first. Function second. Finishing touches later.

Questions to ask before you sign

Before you agree to any financing plan, ask these questions plainly:

- Can I comfortably make this payment every month?

- Is the furniture worth owning after the payments are over?

- Is the offer truly promotional, and what happens if I miss the payoff date?

- Will this new account affect other financial plans I have coming up?

- Am I financing need, quality, and fit, or just impatience?

A simple decision rule

If the furniture is long-term, the payment is safe, and the terms are clear, financing can be a sound choice.

If the furniture is temporary, the budget is tight, or the terms feel fuzzy, don’t do it.

Here’s the answer to “is financing furniture a good idea.” It depends less on the furniture store and more on whether you’re acting like a buyer with a plan.

The Watts Way Financing Quality and Customization

Smart financing should open the door to better decisions, not weaker ones.

That matters most when you’re buying pieces that are customized, built with better materials, and expected to live in your home for a long time. Financing has real value when it helps you choose furniture that fits your house correctly, suits the way your family lives, and avoids the churn of replacing lower-quality pieces again and again.

Why quality changes the financing conversation

A financed purchase should still make sense years from now.

That’s why I draw a hard line between financing disposable furniture and financing lasting furniture. A custom recliner, a solid wood dining set, or a better mattress is different from a trendy filler piece that may not survive a move, kids, or daily use.

When the furniture is chosen carefully, financing can support:

- Custom furniture with fabric, leather, or finish choices that suit your home

- American-made furniture that prioritizes stronger materials and longer life

- Whole-room planning so the pieces work together instead of being bought in isolation

- Professional delivery and setup that protects the purchase from day one

Why service matters too

Financing shouldn’t only help you afford the product. It should help you afford getting the decision right.

That’s where local expertise matters. Good furniture buying isn’t only about price tags. It’s about scale, fabric performance, room flow, color harmony, and whether a piece will still work when your life changes. That’s why strong retailers offer more than a sales floor.

For shoppers who want guidance, the best model includes:

- Complimentary in-store design help for fabrics, finishes, and color direction

- Premium design service with space plans and mood boards, with the deposit credited back toward the purchase

- White-glove delivery and setup

- A service request and support hub after the sale

Better furniture buying starts with fewer guesses.

That’s also why customization matters so much. A chair or sectional that’s sized right and upholstered in the right material tends to stay loved longer. It reflects your home, not a mass-produced catalog.

If you’re exploring how customized pieces come together, custom furniture made simple gives a helpful look at how fabric, finish, and style choices shape the final result.

For buyers in LaGrange and nearby communities, that’s the strongest case for financing. Not convenience alone. Long-term value with a better fit.

Common Questions About Financing Your Furniture

A few questions come up almost every time someone starts thinking seriously about financing furniture.

Will applying affect my credit score

Sometimes yes, sometimes not. It depends on the financing provider and how they check eligibility.

Some options begin with a lighter screening process, while others may involve a harder credit check tied to a new account. The safest move is to ask before you apply. Don’t assume. Know whether you’re just checking options or authorizing a full application.

Can I finance custom furniture

In many cases, yes.

That matters because some of the best purchases are special-order pieces, especially if you’re choosing custom fabrics, leathers, or finishes for a recliner, sofa, or dining set. If you’re ordering a made-for-you piece, ask how the financing lines up with production timing, delivery, and final paperwork.

Can I pay off furniture financing early

Often you can, and that’s a great strategy when the terms allow it.

If your income varies through the year, or you expect a bonus, tax refund, or another cash influx, early payoff can reduce risk and simplify your budget. But don’t guess. Confirm whether there are any prepayment rules before you sign.

What happens if I need service or support after delivery

Local service matters more than people think.

Furniture isn’t a pair of shoes you drop on the porch and forget. It gets delivered, placed, assembled, used, and occasionally serviced. Before financing any major purchase, ask who handles post-sale questions, how support requests work, and what happens if there’s a problem with the item after delivery.

Should I finance a whole room at once

Only if the room contains core pieces you really need and the total payment stays comfortable.

For many buyers, it’s smarter to finance the foundation first. That usually means seating, sleep, dining, and high-use storage. Decorative extras can come later. A finished room feels good, but peace of mind feels better.

If you want answers to common process questions before you buy, the furniture financing and shopping FAQs are worth reviewing.

The plain answer is still the same. Is financing furniture a good idea? Yes, when it helps you buy lasting quality with terms you understand and payments you can handle. No, when it becomes a shortcut to overspending.

If you want neighborly guidance instead of sales pressure, visit Watts Furniture & Mattress, a trusted furniture store LaGrange GA families have relied on for over 65 years. Whether you’re shopping for Mattresses LaGrange GA, Custom La-Z-Boy recliners, Bassett recliners, Serta mattresses, or durable American-made furniture for a full-room update, you’ll find expert help at every step. Visit the Watts showroom at 212 Commerce Avenue in LaGrange to experience the comfort of La-Z-Boy in person. Ready to transform your space? Book a consultation with the Interior Design Center today and let the team help you curate a home you’ll love, with complimentary in-store design advice, premium planning services, and white-glove delivery that takes the guesswork out of the process.