Find Your Perfect Mattress with Our Guides

Furniture No Interest Financing: Your 2026 Guide

You've picked out the sofa, the bedroom set, or the mattress that finally feels right. Then you look at the total and start doing mental math. Should you wait a few more months, settle for something cheaper, or find a way to bring it home now without wrecking your monthly budget?

That's where furniture no interest financing can help. Used wisely, it lets you spread out a large purchase while keeping your home project moving. Used carelessly, it can become confusing fast.

A lot of shoppers are in this same spot. In a 2022 consumer trends study, 30% of Americans who purchased furniture in the prior year said they used a financing option (Provoke Insights furniture trends study). That tells you something important. Financing isn't just for emergencies or oversized remodels. It's become a normal part of buying furniture.

Furnish Your Dream Home Now Not Later

Sometimes the main challenge isn't choosing what you want. It's figuring out how to pay for a room full of quality pieces at one time.

A family in LaGrange may need a new sectional, dining set, and mattress within the same season. A first-time homeowner in West Point may want to stop living out of folding chairs and hand-me-downs. A couple in Pine Mountain may finally be ready for custom furniture that fits their home instead of whatever happens to be in stock online.

That's the practical appeal of furniture no interest financing. It gives you a way to match the timing of your payments to the timing of your life. Instead of delaying the whole project, you can make progress now and pay over time.

Why this matters for real homes

Furniture buying is rarely just about one item. It often happens during a move, a renovation, a new baby, a guest room update, or a decision to replace worn-out pieces all at once.

When that happens, financing can do a few useful things:

- Protect cash flow so you don't empty savings for one purchase

- Help complete the room instead of buying pieces one at a time that don't work together

- Make better quality possible so you can invest in furniture built for generations, not just a few seasons

- Reduce rush decisions because you're planning payments, not just reacting to sticker shock

For shoppers trying to furnish a full space, it also helps to think beyond the single item. A room should function well, fit the layout, and feel finished. If you're working through a larger move or whole-home setup, this guide on how to furnish a new home is a useful companion to the financing conversation.

Good financing should support a smart home plan. It shouldn't pressure you into buying more than you can comfortably repay.

The right mindset before you sign

The healthiest way to think about financing is simple. Treat it like a tool, not a shortcut.

If the payment fits your budget, the terms are clear, and the furniture is worth owning for years, financing can be a solid move. If the agreement feels fuzzy or the payment only works if everything goes perfectly every month, it's time to slow down and ask more questions.

What No Interest Financing Really Means

The phrase no interest financing sounds simple, but shoppers often assume it means the same thing every time. It doesn't.

At its most basic, it means you're allowed to pay over time without paying interest during a promotional period, as long as you meet the plan's rules. This splits a large bill into scheduled pieces instead of paying the whole amount on day one.

The simple version

If you buy a piece of furniture under a 0% APR financing offer, the monthly payment is often just the amount financed divided by the number of months in the promotion. Some larger purchases may also require a down payment of up to 20% (Rooms To Go financing terms).

That matters because the offer may sound easy at first, but the actual monthly commitment can still be meaningful. A longer term usually lowers the monthly burden. A required down payment changes the cash you need right away.

Here's the plain-language idea:

| Plan feature | What it means for you |

|---|---|

| Promotional term | The number of months you have to pay under the offer |

| Monthly payment | Usually based on the financed balance divided across the term |

| Down payment | Money you may need upfront before financing starts |

| APR after promotion | What may apply later, depending on the plan type |

Why people get confused

Many shoppers hear “no interest” and assume three things:

- The payment will be small

- Any remaining balance is no big deal

- Every 0% offer works the same way

Those assumptions cause trouble.

Some plans are straightforward and predictable. Others are strict about timing, and the consequences for missing the payoff deadline can be expensive. That's why the wording matters so much.

A local shopper comparing a living room sectional, Bassett recliners, or even Mattresses LaGrange GA options shouldn't just ask, “What's the monthly payment?” They should also ask how the promotion is structured and what happens if there's a balance left at the end.

What to focus on first

Before you worry about approval, look at the bones of the offer:

- How long is the promotional period

- Is a down payment required

- What exact monthly payment clears the balance in time

- What happens if you pay late or finish late

If you want to review a store's available plans before visiting, a financing page like Watts financing options can help you see the general path before you sit down to apply.

Practical rule: If you can't explain the payment terms back in your own words, don't sign yet.

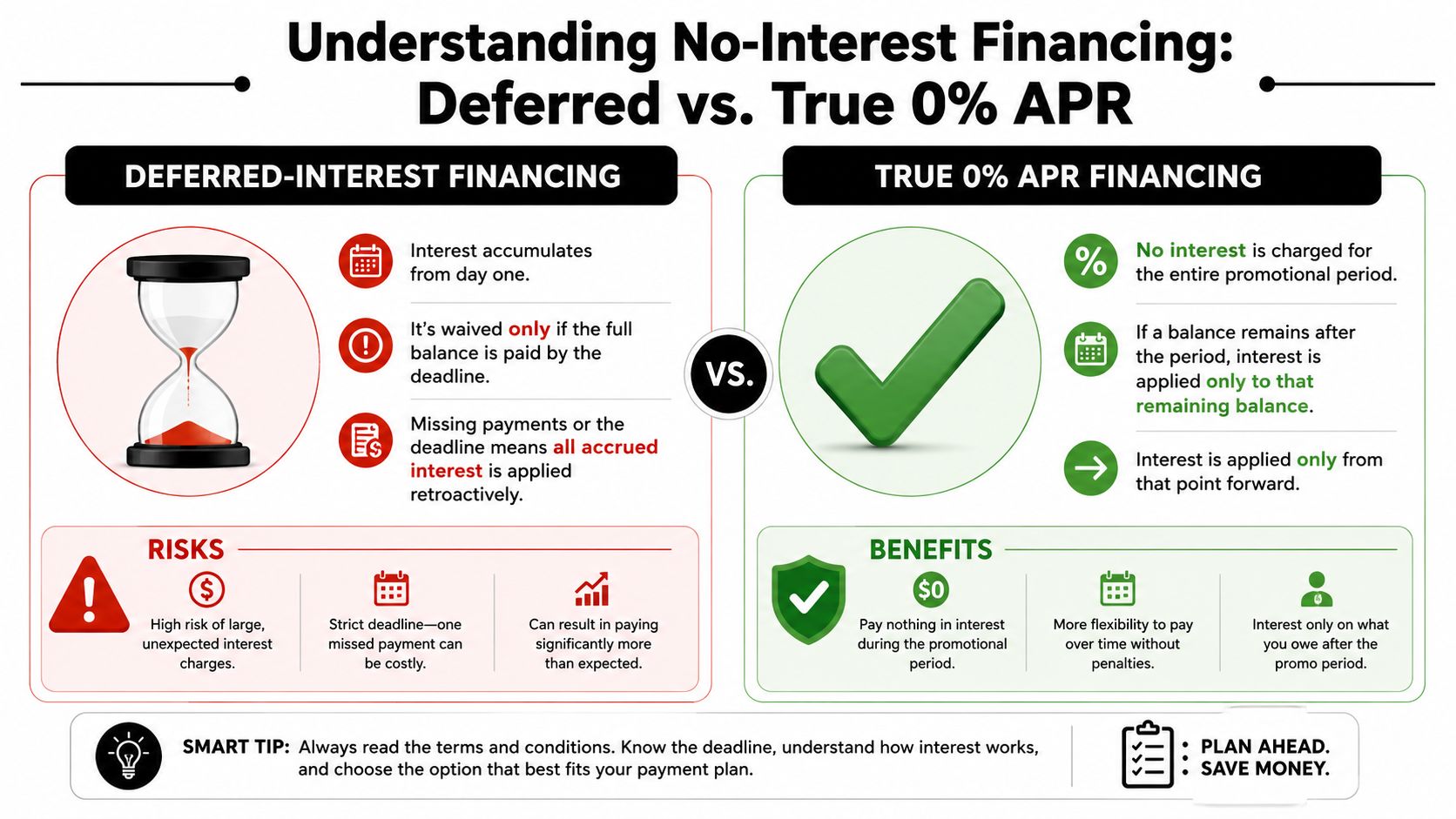

The Two Types of No Interest Plans Explained

A lot of shoppers hear the same phrase, “no interest,” and assume every offer works the same way. At a real store counter, that is where confusion starts.

There are two common plan types. One works like a bill with a clear interest-free window. The other works more like a timer. If the balance is not cleared by the end, the cost can change fast.

Deferred interest financing

With deferred interest, interest is sitting in the background from the purchase date, even though you do not see it added during the promo period. Pay the full balance by the deadline, and that interest is waived. Miss the deadline by even a small amount, and the lender may add interest back to the original purchase date.

That is why this plan catches people off guard. The monthly payment can look manageable, the room can be delivered, and everything can feel on track. Then one leftover balance at the end changes the math.

At a local retailer like Watts, this matters in practical terms. If you are financing a custom La-Z-Boy sectional for a room you want finished before the holidays, deferred interest can work well if you already know the exact monthly amount needed to finish on time. If you are guessing, it is a riskier fit.

True 0% APR financing

A true 0% APR plan is usually easier to follow. During the promotional period, no interest is charged. If you still have a balance after that period ends, interest applies from that point forward on what remains. It does not reach back to day one.

Many shoppers prefer that structure because it is easier to explain in plain English. You still need to pay on time. You still need a plan. But the consequences are usually easier to see coming.

Side-by-side comparison

| Feature | Deferred interest | True 0% APR |

|---|---|---|

| Interest during promo period | Accruing in the background | Not charged |

| If paid in full on time | Accrued interest is waived | No interest owed for promo period |

| If balance remains at deadline | Interest may be added back to the purchase date | Interest starts on the remaining balance from that point forward |

| Best for | Shoppers with a strict payoff plan | Shoppers who want a simpler cost structure |

| Main concern | Missing the payoff deadline | Carrying the balance past the promo term |

Questions to ask before you sign

The safest shoppers are not the ones who memorize finance terms. They are the ones who ask clear questions and wait for clear answers.

Use these at the sales desk:

- Is this deferred interest or true 0% APR

- If I still owe money at the end, does interest go back to the purchase date

- What monthly payment gets this paid off within the promo period

- Is the minimum payment enough to clear the balance on time

- What happens if I pay late once

Those questions help whether you are buying one recliner or furnishing a full room. They also help you match the financing plan to the home you are trying to build, instead of choosing a plan first and hoping it fits later.

If you want to compare promotional financing with installment-style offers before visiting the store, this guide to buy now pay later furniture options gives a useful starting point.

A good financing offer is not just about the headline. It is about whether you can explain the rules, the deadline, and the payoff amount without rereading the contract.

A quick store-floor example

Say a family in LaGrange finds the sectional they have wanted for years. The room layout is right. The fabric is right. The monthly minimum payment looks fine.

The smart next question is not “Can we afford the minimum?” It is “What do we need to pay each month to own this piece without surprises?”

That one question separates a helpful financing tool from an expensive misunderstanding.

Avoiding Common Financing Traps and Fine Print

A financing plan can look simple on the sales tag and feel very different once the paperwork starts. That is why careful buyers slow down here. They are not being difficult. They are protecting the budget they worked hard to build.

At a local store, this matters in practical ways. A family may be picking out a custom La-Z-Boy sectional for the room they plan to use every night. The goal is not just getting furniture home this week. The goal is getting the right piece home without turning a smart purchase into an expensive surprise.

Trap one. Letting the minimum payment set the plan

Minimum payments keep the account in good standing. They do not always get the balance paid off before the promotional period ends.

That difference causes trouble. It is a little like paying only the amount needed to keep the lights on while expecting the whole utility bill to disappear. The account stays active, but the balance can still be there when the deadline arrives.

How to avoid it

- Ask for the monthly amount that pays the full purchase off within the promo period

- Check the final promotional month in writing

- Round up your payment so taxes, fees, or small balance leftovers do not stay behind

Trap two. Leaving even a small balance at the end

This is the fine-print moment that catches people off guard. On some deferred-interest plans, a leftover balance at the deadline can trigger interest charges tied back to the original purchase period.

A shopper may think, "We only missed it by a little." The contract may treat that very differently.

Watch closely: "Almost paid off" and "paid off" can lead to two very different outcomes.

This is one reason experienced sales teams at stores like Watts walk customers through the calendar, not just the monthly figure. A good plan should fit the actual payoff date, not just look comfortable on the first bill.

Trap three. Assuming every part of the purchase qualifies

Financing offers do not always apply to every item in the order the same way. A room package might include in-stock furniture, a special-order piece, protection coverage, delivery, or accessories. One part may qualify for the promotion while another part follows different terms.

That can change both your payment plan and your expectations.

Use this checklist before you sign:

- Covered items. Confirm exactly which products are included in the offer.

- Promo start date. Verify whether the clock starts on purchase, delivery, or account opening.

- First payment date. Make sure the schedule gives you enough time to finish before the deadline.

- Amount due today. Clarify any down payment or deposit required at checkout.

Trap four. Using financing to stretch past your real budget

Financing works best as a tool, not a reason to buy more than the household budget can handle. A larger sectional, upgraded leather, or extra bedroom set may look manageable when the payment is broken into smaller pieces. The better question is whether that payment still feels comfortable after groceries, utilities, and the rest of monthly life show up.

That is why it helps to review practical guidance on how to finance furniture without budget surprises before you apply.

A good financing choice should support your home plan. If the numbers feel hard to explain, hard to track, or hard to pay off on time, pause and ask for cleaner terms.

Your Trusted Financing Options in LaGrange GA

For shoppers in LaGrange, Troup County, West Point, Pine Mountain, and Hogansville, financing works best when it's tied to a clear home goal. Maybe that's a custom La-Z-Boy recliner in the right fabric. Maybe it's American-made furniture in solid wood. Maybe it's replacing an aging mattress with a more supportive sleep setup without paying the full amount all at once.

That's where transparent terms matter more than flashy wording.

Financing should match the furniture you're buying

There's a big difference between financing a quick replacement piece and financing something made for long-term use.

Higher-quality furniture often brings options that matter over time:

- Customization such as fabric, leather, or finish choices

- Better construction for everyday use

- Design coordination across more than one room

- White-glove delivery and setup so heavy pieces are handled properly

That's one reason local buyers often pair financing with a more thoughtful purchase. They're not just asking, “Can I get this today?” They're asking, “Will this work in my home for years?”

How this connects to local service

At Watts Furniture & Mattress, shoppers can review monthly payment options as part of the buying process while also looking at custom-order furniture, mattresses, and room planning support. That can be useful for people who want one conversation about the furniture, the payment structure, and the layout of the room.

The design side matters here, too. Complimentary in-store design help can make it easier to pull together fabrics and colors. For larger projects, a premium design service with space planning and mood boards can help you avoid buying pieces that don't fit the room or each other.

Financing works better when you know exactly what you're building, not just what you're buying.

A better use of financing

The strongest use of furniture no interest financing is often this: using it to buy fewer, better pieces that fit your home well instead of filling a room with placeholders.

That might mean:

- A Bassett dining set with the finish you want

- A La-Z-Boy sectional configured for your floor plan

- Serta mattresses selected with comfort guidance instead of guesswork

- Case goods and upholstery that reflect your home, not a mass-produced catalog

That approach won't fit every budget. But if you're financing at all, it's worth asking whether the plan helps you buy furniture you'll still be glad you chose years from now.

A Step-By-Step Guide to Getting Approved

Approval is the part many people dread most. They assume it will be awkward, complicated, or all-or-nothing.

In practice, the process is usually more straightforward than people expect. And not every shopper is walking in with the same credit history, income pattern, or household needs.

What lenders usually look at

Many promotional 0% APR offers do depend on credit qualification. At the same time, the market has expanded to include more flexible options for shoppers with thinner credit files or less traditional borrowing histories (overview of flexible furniture financing paths).

That doesn't guarantee approval. It does mean you may have more than one path.

A retailer or financing partner may review things like:

- Identity details such as name, address, and contact information

- Basic financial information used for eligibility review

- Credit history, depending on the offer

- Purchase size, which can affect the plan options shown

What the process often looks like

For most shoppers, the application path feels like this:

Choose the furniture first

It's easier to evaluate financing when you know whether you're buying one recliner, a full bedroom set, or several rooms at once.Review the available plans

Ask which offers are promotional, which are standard installment options, and whether qualification changes the terms.Submit the application

This is usually done in-store or online, depending on the retailer and financing partner.Read the approval terms carefully

Don't stop at “approved.” Look at the payment schedule, any required down payment, the promo length, and what happens if a balance remains.Set your payment plan immediately

Put the target amount into your budget and automate it if possible.

If you're worried about qualifying

You're not alone. First-time homeowners, renters, and recently relocated families often have questions here.

A few practical moves can help:

- Bring your basic information ready so the process moves smoothly

- Ask whether there are alternative financing paths if the first offer isn't a fit

- Focus on payment comfort, not just approval

- Shop in person if you want guidance rather than trying to decode terms alone

For many people in LaGrange and nearby communities, talking through the options face to face lowers the stress. That's especially true when the purchase includes custom furniture, room planning, or several categories at once.

Start Building Your Dream Home Today

Furniture no interest financing can be a smart tool. The key is knowing exactly what kind of plan you're using and what the payoff rules require.

If you remember only three things, remember these:

- Not all no-interest offers work the same way

- Deferred interest carries more deadline risk

- The right plan should fit both your budget and your home goals

That's especially important when you're buying furniture meant to last. A well-made sectional, a supportive mattress, or a solid wood dining set can improve daily life for years. Financing can help you get there sooner, but only if the terms are clear and the payment is realistic.

The best buying decisions usually come from a mix of patience and clarity. Read the agreement. Ask direct questions. Match the plan to your budget. Then choose pieces that belong in your home.

Visit Watts Furniture & Mattress at 212 Commerce Avenue in LaGrange to experience the comfort of La-Z-Boy in person. Ready to transform your space? Connect with the Interior Design Center for complimentary in-store guidance or ask about premium design support with space planning and mood boards, with the deposit credited toward your purchase.